The Southeast is becoming the physical map of the AI economy.

The region has land, power corridors, fiber routes, ports, business-friendly state governments and fast-growing metros. It also has rural counties looking for tax base, utilities trying to plan for unprecedented load growth and communities beginning to ask whether the new industrial prize is worth the tradeoffs.

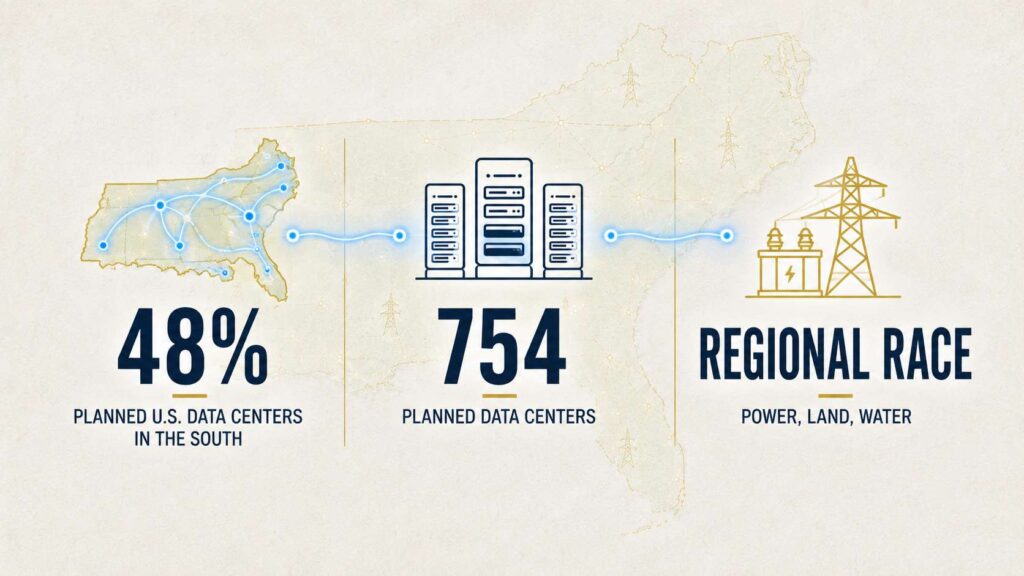

This is not just a Georgia story. It is a regional race.

The Pew Research Center reported in April 2026 that the South accounts for 48% of planned U.S. data centers. Pew found 754 planned data centers in the South, compared with 1,209 existing ones, and said Virginia, Texas and Georgia lead the country in planned data centers.

The geography of computing is moving toward the places that can offer the fastest route to power.

That is the opportunity. It is also the pressure point.

Northern Virginia is the preview

Any serious Southeast data center story starts in Northern Virginia.

Loudoun County and the surrounding region became the world’s most famous data center cluster because of early internet infrastructure, fiber density, proximity to federal and enterprise customers, and aggressive data center investment. It is still the dominant U.S. market.

Loudoun County’s 2026 data center property statistics list 251 data center parcels, more than 44 million square feet built and more than 9.2 million square feet under construction as of Jan. 1, 2026.

That scale is why Northern Virginia is both model and warning.

The model is obvious: data centers can become a huge tax-base engine. They can turn industrial and exurban land into high-value property. They can anchor a national reputation for digital infrastructure.

The warning is just as important: once a region becomes deeply dependent on data centers, the public debates become harder. Transmission lines, land values, noise, water, power availability, local zoning and tax policy all become tied to one industry.

Georgia is not Northern Virginia yet. But Atlanta is now large enough to learn from it before the decisions become irreversible.

Georgia is now a front-tier market

Georgia has moved into the top tier quickly.

CBRE reported that Atlanta ended 2025 as the second-largest U.S. data center market by inventory, behind Northern Virginia. Pew’s national analysis counted 94 operating data centers and 141 planned data centers in Georgia as of Feb. 19, 2026.

The companies behind the Georgia buildout include familiar names: Google in Douglas County, Microsoft in Douglasville, Palmetto and East Point, AWS in Butts and Douglas counties, T5 in Lithia Springs and South Fulton/Palmetto, QTS in Atlanta and Fayetteville, plus DC BLOX, Flexential, CoreSite and others.

The Georgia story is more than recruitment. It is now policy.

Georgia Power’s 2025 Integrated Resource Plan projects 8,500 megawatts of electrical load growth over six years. The Public Service Commission says 9,985 megawatts of new energy generation were certified in December 2025, with about 80% expected to power data centers. Local governments around the state are passing ordinances and moratoriums. A state audit has reopened the debate over whether Georgia’s data center tax exemption is still worth its cost.

That makes Georgia one of the most important data center policy laboratories in the country.

More From This Series

North Carolina shows the backlash spreading

North Carolina is another major Southeast technology state, with the Research Triangle, Charlotte, Apple, Google, financial services and a long history of recruiting large technology projects.

But even there, data center opposition is gaining momentum.

Axios Raleigh reported in April 2026 that moratoriums were expanding across the state, including Orange County and Apex, with Durham considering a two-year moratorium. The concerns are familiar: electricity costs, water use, noise and aesthetics. Axios also reported that Chatham County was being sued by a developer over a moratorium and that Gov. Josh Stein had called for lawmakers to review data center tax breaks.

That is the regional pattern.

Communities are not necessarily rejecting technology. They are rejecting uncertainty. When a project arrives with enormous power demand, limited public disclosure and a small permanent workforce relative to investment size, local governments want time to rewrite rules.

Georgia counties are doing the same thing.

Tennessee shows the environmental justice fault line

The most nationally visible Southeast data center controversy may be in Memphis.

Elon Musk’s xAI has built the Colossus AI data center in South Memphis, a community already burdened by industrial pollution concerns. The controversy has centered on gas turbines, air permitting and allegations from environmental advocates.

Data Center Dynamics reported in 2026 that xAI received permits for gas turbines at the Memphis data center, while the Southern Environmental Law Center had accused the company of Clean Air Act violations tied to turbine use. The article also reported that SELC and the NAACP had announced intent to sue over possible violations.

The Memphis story matters beyond Tennessee because it shows what can happen when AI infrastructure moves faster than public trust.

It also raises a difficult regional question. If data centers cannot get power from the grid quickly enough, will more operators turn to behind-the-meter gas generation, temporary turbines or other on-site power solutions? If so, which communities will host that generation, and who will measure the health impact?

For the Southeast, power is no longer just an economic development issue. It is an environmental justice issue.

Mississippi shows the rural mega-project model

Mississippi represents another version of the regional story.

AWS announced plans for a $10 billion investment in Mississippi, described by the company as the largest capital investment in the state’s history. The project involves multiple data center complexes in Madison County industrial parks and is projected to create at least 1,000 jobs.

The announcement fits the new rural data center model: large industrial sites, major state and local coordination, workforce training promises, tax-base expectations and a company tying cloud and AI demand to local economic development.

For rural and exurban counties, the appeal is obvious. A data center project can dwarf the size of normal local economic development wins. It can bring new infrastructure, construction activity and a stronger tax base.

The risk is also obvious. Smaller governments may have less technical capacity to evaluate power, water, sewer, road, emergency and fiscal assumptions. They may be asked to approve projects whose long-term impacts are difficult to model. If incentive agreements, utility obligations or community benefits are not transparent, residents may not know what was traded until years later.

The Southeast is building a network, not isolated campuses

It is tempting to look at each data center as a separate local project. That misses the regional network.

DC BLOX’s footprint, for example, includes Atlanta, Birmingham, Huntsville, Chattanooga, Greenville, High Point, Myrtle Beach and other Southeast locations. CoreSite’s Atlanta facilities connect customers to major cloud platforms. Google’s Douglas County site, Microsoft’s Georgia campuses, AWS’s Georgia and Mississippi investments, and T5’s Atlanta campuses all sit within a larger Southeast infrastructure geography.

The region is not simply adding buildings. It is becoming an interconnected compute, fiber and power zone.

That should change how the Southeast talks about economic development. States are competing against each other, but they are also facing the same questions: how to price power, how to protect residential ratepayers, how to manage water, how to regulate backup generation, how to handle local opposition, and how to make sure workforce programs reach residents near the projects.

What Georgia can learn from the region

Georgia does not have to invent the answer alone.

Northern Virginia shows the revenue upside and the danger of overdependence. North Carolina shows that even tech-friendly communities will push back when local rules feel outdated. Memphis shows the environmental justice risk when power needs move faster than permitting trust. Mississippi shows the scale of rural recruitment and the importance of negotiating durable public benefits.

The Southeast data center race is real. But the best-positioned states will not simply be the ones that approve projects fastest.

They will be the ones that can say yes with confidence: yes to infrastructure, yes to transparency, yes to ratepayer protection, yes to water planning, yes to local workforce development and yes to communities having enough information to understand what is being built around them.

That is the next phase of competition.

The winners will not just have the most megawatts. They will have the best public bargain.

Sources

- Pew Research Center: Most new data centers in the U.S. are coming to rural areas

- CBRE: Atlanta Emerges as One of North America’s Fastest Growing Data Center Hubs

- Loudoun County 2026 Data Center Guidelines

- Axios Raleigh: Data center opposition is growing in North Carolina

- Data Center Dynamics: xAI gas turbines in Memphis

- AWS Mississippi investment announcement

- DC BLOX Atlanta Data Centers